20 Up-and-comers To Watch In The Reverse Mortgage Industry

Unknown Facts About Mortgages

That's why we provide features like your Approval Chances and cost savings quotes. Obviously, the offers on our platform do not represent all monetary items out there, but our objective is to show you as lots of fantastic options as we can. Whether it's the familiar environment, the surrounding community or the emotional worth of the house itself, numerous reasons contribute to elders wanting to stay in their homes for as long as possible.

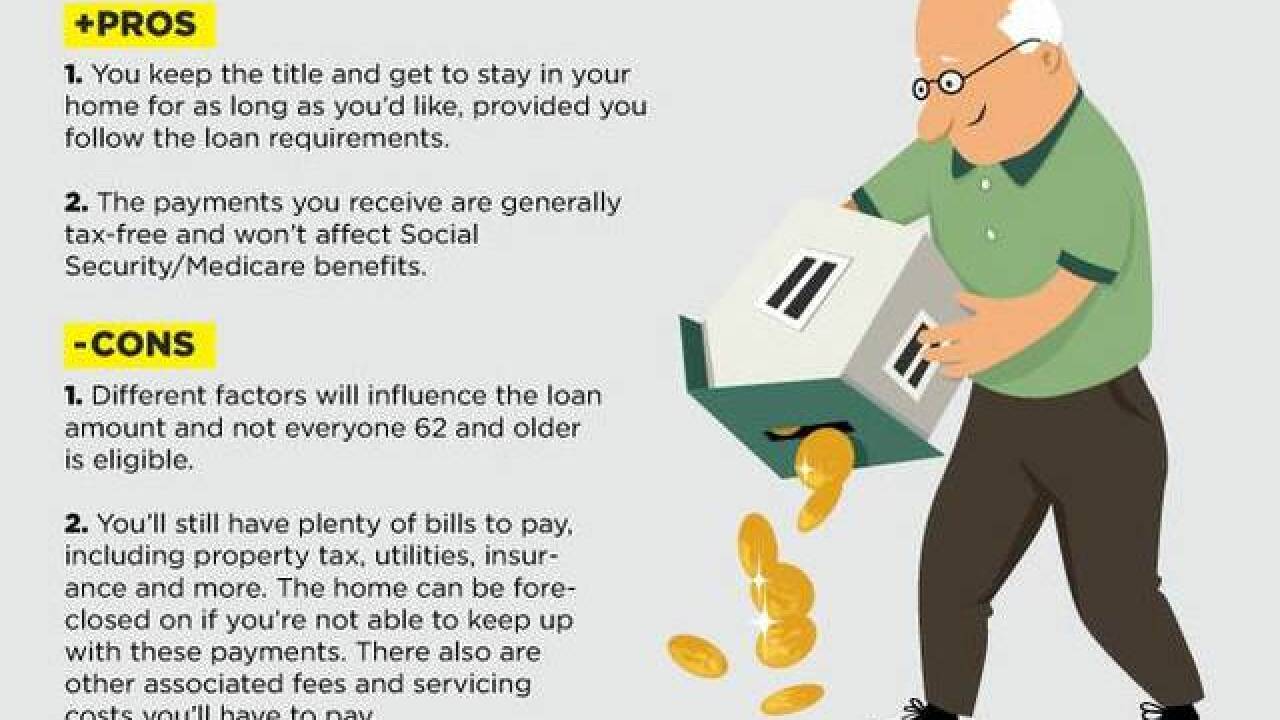

Reverse home loans are loans that permit senior citizens to tap into the home equity they've constructed without needing to sell their property. And unlike standard loans, where you make regular monthly payments against the principal and interest, with a reverse home loan you only repay the principal and interest once you offer or move completely from the home.

If this is the case, you probably own a large percentage if not all of your home. The current market worth of your house minus what you still owe on the home (if anything) is called your equity. To learn just how much equity you have in your house, deduct the remaining balance of your home loan (the quantity you still owe to the lending institution) from your house's current value. To certify for a house equity conversion mortgage, the most common kind of reverse mortgage, you must be at least 62 years old and either own your house outright or have a home mortgage with a low balance, together with satisfying a number of other requirements, like the home being your principal home and remaining so.

4 Easy Facts About Residential Mortages Explained

There are a couple of methods you can take the loan, including as one swelling amount in advance, as a line of credit that you make use of as required until you've consumed the line of credit, or as regular monthly payments. Reverse home mortgages normally have variable rates of interest, however house equity conversion mortgages can use fixed rates.

Rather, you are accountable for repaying the loan when you move completely or offer the house. Or your estate can settle the loan once you pass away. This all noises pretty good, right? Just bear in mind that while you're not accountable for paying principal or interest on a monthly basis, you are responsible for keeping existing with your home taxes, house owners insurance and property maintenance.

Now that we've got the essentials down, let's go into the details. There are 3 kinds of reverse home loans: single-purpose, proprietary and home equity conversion mortgage. If you need money for a particular purpose, like a house improvement, a single-purpose reverse mortgage might be a good option for you. These loans are used by some nonprofits and state and local federal government firms to allow borrowers to do things such as preserve their residential or commercial properties, make medically necessary house improvements like wheelchair ramps, or pay their real estate tax.

What Does Reverse Mortgage Mean?

Single-purpose reverse mortgages tend http://edition.cnn.com/search/?text=reverse mortages to cost less than other reverse home loan choices, but they are likewise the most elusive as they're just available through certain state and regional government companies and nonprofits. Contact local senior resources, like a Location Firm on Aging, to see if they have any information about single-purpose reverse home mortgages offered in your area.

Usually, it can be used for any purpose. Considering that it's a private loan, it's not subject to the very same dollar constraints as you see with home equity conversion home loans, however you may pay more for it. That could imply a greater loan amount if you have a high-value home. Among the downsides of exclusive reverse mortgages is that they tend to have greater costs.

Likewise, bear in mind that the loan terms vary from loan provider to lender. So store around and compare different loan amounts, costs and terms. And even if the lenders do not require you to see a monetary http://bettydriscollcorbinx0ay.yousher.com/15-best-twitter-accounts-to-learn-about-mortgages-and-divorce counselor, it's probably a great idea to have a neutral 3rd http://www.bbc.co.uk/search?q=reverse mortages party discuss the benefits and overall yearly expenses of each choice.

The Of Reverse Mortgage

The loans can be utilized for any function and often have lower costs than proprietary reverse home mortgages. But because these are federally insured loans, the requirements can be more stringent and more streamlined. Here are some of the HECM eligibility qualifications: The customer must be 62 years or older Your home should be your primary home Your home need to be a single-family house, HUD-approved apartment project, made home that meets FHA requirements, or a two- to four-unit structure where you inhabit one system You own your house outright or have a low sufficient home loan balance that you can pay it off with the loan continues You have the financial means to continue spending for your real estate tax, homeowners insurance coverage, repair work and upkeep on your home, and house owners association fees, if relevant You're not overdue on any federal debt You must go to a federally authorized financial therapist, who will explain the HECM procedure, requirements, expenses and loan alternatives to you Your loan quantity is http://query.nytimes.com/search/sitesearch/?action=click&contentCollection®ion=TopBar&WT.nav=searchWidget&module=SearchSubmit&pgtype=Homepage#/reverse mortages based upon the reverse mortgage after death age of the youngest customer (or eligible nonborrowing spouse), your home's worth (or the optimum claim quantity or list prices, whichever is less), and the rates of interest.

No matter your house's worth though, the maximum amount you can obtain with an HECM is $679,650. However even if your house is worth $679,650, you won't always receive the full amount. Reverse home mortgages are complex agreements that can have alarming implications for your future if you don't plan properly.

A financial counselor can assist discuss the details of your loan so that you can make the best decision. Before choosing a reverse home mortgage, request for an in-depth schedule of the total expenses related to the loan, with a breakdown of which costs will be collected upfront and which will be collected throughout the regard to the loan.

The Facts About Mortgages Uncovered

Home mortgage insurance premium: This is to pay for FHA mortgage insurance coverage. You will be charged a preliminary MIP at closing equal to 2% of the loan amount. Then you will be charged 0.5% of the impressive loan quantity yearly. The cost of MIP is normally consistent among loan providers. Third-party costs: To determine your house's worth (and by extension, your equity), your lender might require you to get, and pay for, an appraisal.

Third-party expenses and requirements can vary in between lending institutions, so make certain to compare your alternatives. Origination charge: The lending institution will charge you an origination charge for processing the loan. The origination cost can be the greater of $2,500 or 2% of the first $200,000 of your home's worth, plus 1% of the quantity over $200,000.