Common-Sense Secrets Of Personal Debt - Locating Guidance

The Best Strategy To Use For Get Out Of Debt

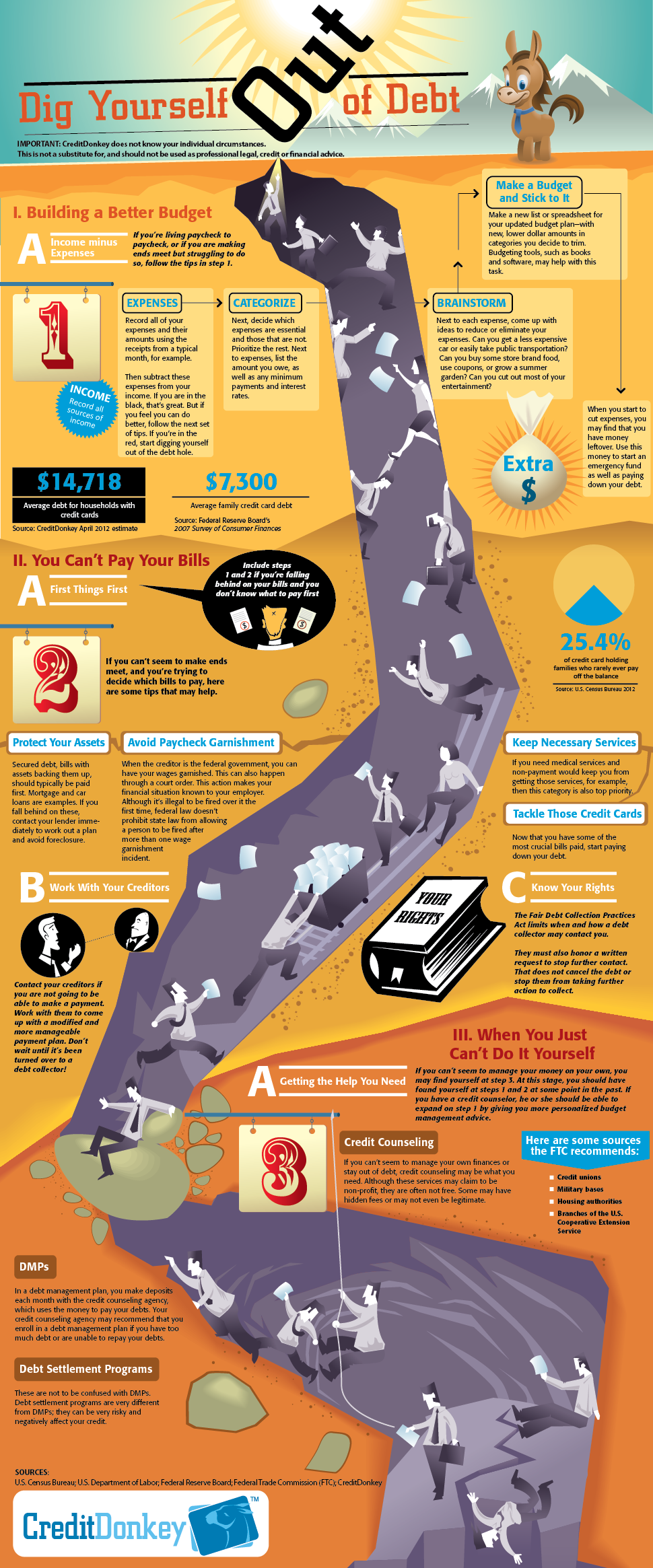

= percentage of total debt owed overall debt Example: auto loan-- total debt = $1,145.39/ $3,380.69 = 0.34 or 34 percent To figure out the amount you can pay on each debt, make this calculation: total quantity can pay X percentage of overall debt owed = amount can pay on that debt Example: $300 X. 34 = $102 Method 3.

Financial obligations Amount owed Amountrequired Proratedpayment Vehicle loan $1,145.39 $180 X. 50 $90.00 Bank card 680.30 35 X. 50 17.50 Bank loan 525.00 170 X. 50 85.00 Bank loan 755.00 190 X. 50 95.00 Department store 275.00 25 X. 50 12.50 Totals $3,380.69 $600 $300.00 You have $300 per month offered for debt payments.

Each lender is provided a prorated payment of 50 percent of the routine monthly payment. It is crucial to repay all of the debts you owe. If there is insufficient cash to pay on all of your loans, think about prioritizing your financial obligations. Financial obligations you might wish to pay first include mortgage or lease, utilities, protected loans, and insurance.

Some examples of third top priorities are medical professional, dental professional, and medical facility expenses. Relative and buddies typically want to wait. Utilize the worksheet on page 7 to establish your debt-payment plan. Write the creditor's name in the first column. Figure the portion of overall debt you owe each financial institution and write it in the second column.

The 2-Minute Rule for Get Out Of Debt

Decide if you will pay the debtors in equivalent amounts (Approach 1), by percentages (Method 2 or 3), or according to what action the financial institution may take (such as garnishment or repossession). Compose the dollar amount you can pay each creditor each month in the 4th column. Now that you have worked out a plan, destroy all of your charge card.

Creditors usually are more responsive to your proposal if you take the initiative to call them initially and reveal a genuine desire to pay your commitments. If you can not visit your financial institution, call or compose a letter. A sample letter you can utilize for writing your letter is consisted of in this publication.

In your letter, make certain to consist of the http://junestarkweatherdaltonigm8.unblog.fr/2020/01/28/a-fast-way-to-get-out-of-debt-its-not-as-difficult-as-you-think/ following: Why you fell behind in your payments (such as loss of job, disease, divorce, death in the household, or bad money-management skills). Your existing earnings. Your other obligations. How you plan to bring this debt up-to-date and keep it existing. The specific amount you will be able to repay every month.

If you stop working to follow the plan you and your lenders have agreed upon, you damage your chances of getting future credit. Tell your financial institution about any modifications http://edition.cnn.com/search/?text=debt solutions that may impact your payment arrangement. For very severe debt issues, a nonprofit credit therapy agency might have the ability to even more negotiate lower regular monthly payments or interest.

Get Out Of Debt Can Be Fun For Everyone

Consumer Credit Counseling Provider (CCCS) firms in Mississippi consist of Finance International (statewide), http://www.bbc.co.uk/search?q=debt solutions Household Service Firm (Southaven), and Cred Capability (Jackson and statewide). Bankruptcy might be the last hope in handling debt. The Federal Insolvency Code provides two types of debtor relief. Chapter 7 of the code is the straight insolvency provision and offers liquidation (convert into cash) of the debtor's properties.

Mississippi law lets the debtor keep specific home, and all other financial obligations are released in bankruptcy. With insolvency under Chapter 7, you give up the home you put up for security when using credit unless the debts are reaffirmed by court permission and you continue to pay the financial institution. Chapter 13 is the wage-earner's strategy.

While paying the debts, you will have the ability to keep the important things you purchased on credit if the courts approve your strategy. Modifications in personal bankruptcy laws entered into impact in October 2005. The modifications provide more reward to look for personal bankruptcy relief under https://www.washingtonpost.com/newssearch/?query=debt solutions Chaper 13 rather of Chapter 7. If you have a steady income, Chapter 13 lets you keep property you might otherwise lose.

After you have made all the payments under the plan, you recieve a discharge of your debts. With minimal exceptions, the Bankruptcy Abuse Avoidance and Consumer Defense Act of 2005 requires individuals who prepare to file for insolvency security to get credit counseing from a government-approved organization within 180 days before they submit.